The Large-Block Strategy Is Back: How to Profit from Large-Block IPv4 Arbitrage Today

A Market with a Memory

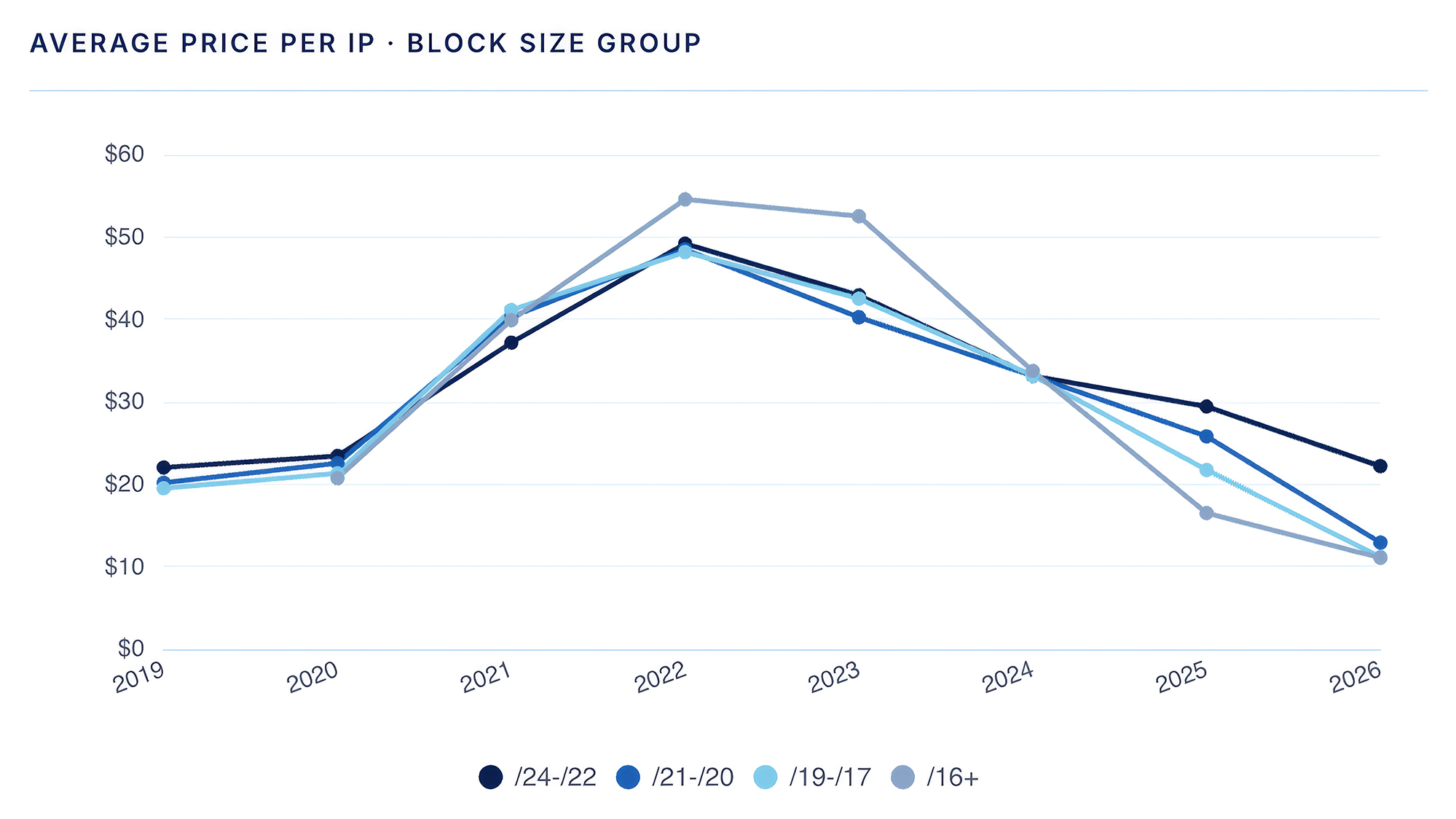

Markets tend to repeat themselves, and the IPv4 address market is no exception. Between June 2020 and August 2021, a notable pricing anomaly took hold: large blocks of IPv4 addresses‚ /16s and larger‚ sold at a measurable discount on a per-address basis compared to smaller blocks like /22s and /24s. The price gap ranged from roughly 2.4% to 17.5% over that period. The logic of commodity markets, where buying in bulk typically commands a discount, seemed to apply: large buyers expected bulk pricing, sellers facing a windfall accepted lower per-IP offers, and the market obliged.

But that discount created an obvious opportunity. A large bundle of addresses was cheaper per IP address than the same block subdivided and sold in pieces. During 2020 and 2021, larger sellers and strategically-minded traders began doing exactly that, breaking up /16 blocks and selling the resulting smaller units at the higher per-address rates the market would bear. The strategy worked, and it worked well, while the window lasted.

The Inversion

That window closed in late 2021 as the price relationship inverted. Large blocks then began commanding a premium, and smaller blocks drifted lower and became more variable in price. For a few years, the large-block-subdivision strategy was no longer applicable. This persisted until mid-2024.

The Transition

The data from IPv4.Global’s marketplace and independent tracking sources tell a clear story. Beginning in mid-2024 and throughout the first half of 2025, large block pricing‚ particularly for /16s and larger, fell sharply. (As predicted.) Average /16 prices dropped from nearly $50 per address in mid-2024 to just over $24 by March 2025, and by mid-2025 had fallen below $20 per address for the first time since 2019. By early 2026, /16+ pricing had declined to under $10 per address on certain transactions, with the broader trend well below $15.

Meanwhile, smaller blocks, /20 through /24, have held comparatively firm, though diverging as well. Smaller blocks in 2025 hovered in the $31 to $34 range, and in ARIN-registered space, even higher. The divergence was stark: where there once was a modest 10-17% gap in per-address pricing between large and small blocks in the 2020 to 2021 window, the spread in 2025 in some cases has been multiples of that, with large blocks available at half the per-address cost of small blocks.

The trend, in terms of multiples, continues today. Blocks from /20s through /24s are more than twice the price, per IP, as /16s. IPv4.Global’s marketplace reporting has noted this dynamic: the current per-IP differential between small and large blocks represents a significant opportunity for sellers. The strategy of subdividing larger allocations into smaller blocks that command marginally higher prices per address has returned as a logical strategy.

Possible Causes

The reason for the dislocation is straightforward. The dominant force pushing large-block prices upward through 2020 to 2022 was hyperscale cloud demand. AWS, Azure, and others were accumulating enormous address inventories for their infrastructure build-outs. Once those buyers largely satisfied their needs, they stepped back from the market. In some cases, these buyers also altered their buying strategy, focusing on direct purchases rather than brokered ones.

The remaining buyer pool, while broad and growing in number, is composed largely of smaller ISPs, hosting providers, and enterprises. These need modest allocations. They are precisely the buyers for small and mid-sized blocks, /22s, /23s, /24s, not /16s. The supply of large blocks, meanwhile, has persisted as legacy holders, universities, telecoms, and restructured organizations, monetize underutilized assets at prices they find acceptable.

The Strategy

The core mechanics of a logical strategy are easy to describe. If you own a /16 (65,536 addresses) or larger block at the current depressed per-address price, do not sell it as such. Subdivide it into appropriately sized smaller blocks, /20s, /22s, /23s, /24s depending on market demand. Sell those smaller blocks at the prevailing higher per-address rate. Benefit from the spread.

Then, if you must, buy a replacement /16 and renumber where necessary. The pain of the renumbering may be more than compensated for by the difference in costs.

In 2020 through early 2021, the price gap of up to 17.5% made this viable despite transaction costs. In the current environment, the gap is substantially larger. Even accounting for costs, and those costs are real and must be carefully modeled, the arithmetic can be compelling.

But this is where the strategy’s real complexity lives: in the costs, the expertise requirements, and the supply of buyers willing to absorb the subdivided blocks.

The Cost Structure: What Eats the Spread

Every transfer in the IPv4 market incurs fees payable to the Regional Internet Registry (RIR) that administers the address block, plus brokerage fees. These vary significantly by region and must be factored rigorously into any arbitrage calculation.

ARIN charges sellers a flat $500 per transfer regardless of block size. Buyers pay a fee that scales with block size. Critically, each subdivision sale is a separate transfer, so breaking a /16 into sixteen /20s means sixteen separate transfer events, each carrying its own $500 seller fee. That’s $8,000 in ARIN seller fees alone on the exit side of a single /16 sale.

RIPE NC is the most favorable environment for this strategy from a pure fee perspective: there are no transfer fees under RIPE NCC, though membership fees apply. For operators already holding RIPE membership, the incremental cost of multiple sub-block transfers is low, making the RIPE region notably attractive for subdivision strategies.

LACNIC requires a $200 initial payment to open a transfer ticket, typically paid by the seller, plus a remaining fee of $1,000 for blocks smaller than /19 and $1,500 for /19 and larger blocks, generally borne by the buyer. Each subdivision transaction requires a separate ticket and opening fee. LACNIC’s paper-based, manual transfer process also tends to run slower, adding time cost and uncertainty to the strategy.

APNIC calculates fees as 20% of the annual membership fee for the number of IPv4 addresses being transferred in a single transfer request. For intra-APNIC transfers, the buyer pays; for inter-RIR transfers, the seller pays. The calculation is somewhat complex and depends on both parties’ membership tiers, but the per-transfer cost for smaller blocks can add up meaningfully when many subdivisions are being sold.

The Expertise Requirement

Beyond fees, executing this strategy requires genuine operational expertise. IPv4 transfers are not simple click-to-complete transactions. Each RIR has its own documentation requirements, verification processes, justification standards, and approval timelines.

ARIN demands documented justification of need and officer attestation. It also enforces a 12-month hold rule preventing the source organization from having received ARIN space in the prior year. RIPE NCC requires clear transfer documentation and signed agreements. APNIC mandates usage plans demonstrating need from recipients. LACNIC’s process is largely manual and can extend for weeks.

Mismatched WHOIS records, incomplete Letters of Authorization, outdated corporate registration details, inconsistent RPKI data, or a block with a disputed history can halt a transfer entirely or stall it for weeks. The more subdivisions being executed, the more opportunities for any one of those issues to create delay, cost, and uncertainty.

For anyone executing this strategy at scale, the operational burden is real. Maintaining clean, synchronized registry and RPKI records across potentially dozens of sub-block transactions requires dedicated attention and expertise that most organizations don’t have internally.

This is the primary reason professional brokerage relationships matter here, not just for finding buyers, but for managing the administrative and compliance machinery of the transfers themselves.

The Buyer Supply Question

Another limiting factor is the depth of the buyer market for the smaller blocks being sold. The strategy only works if there is a pool of buyers willing to absorb sub-blocks at the higher per-address rates, in a reasonable timeframe, without the seller being forced to discount to close.

The good news: the buyer market for small and medium blocks is structurally robust. Transaction data shows that worldwide transfers of blocks smaller than /16 have been remarkably stable, running between 10 to 12 million addresses annually since 2020, with early 2025 suggesting a pace potentially 20% above that norm. Smaller ISPs, cloud-adjacent businesses, hosting providers, and enterprises with targeted needs for /22s and /24s form a persistent, distributed buyer base. Unlike the hyperscale buyers who drove large-block demand in 2021 through 2022 and then dramatically reduced publicly-traded demand in 2024, this buyer pool is not episodic, it represents ongoing operational need.

Matching that buyer pool efficiently, however, requires access to a platform and network with genuine reach. This is where the choice of brokerage channel matters significantly.

The Role of IPv4.Global and Private Sales

IPv4.Global, a division of Hilco Global, operates the world’s largest IPv4 marketplace and has published the most comprehensive historical price data available in this market, making it the reference point for pricing transparency.

For a seller subdivision strategy, two channels at IPv4.Global are particularly relevant. The marketplace, operating as an open auction and listing platform, provides broad exposure and price discovery. But for sellers executing a structured block-subdivision program, the Private Sales channel at IPv4.Global may be an alternative and is sometimes the preferred approach.

Private sales allow sellers to work directly with the IPv4.Global team to match blocks with specific buyers without the full public auction process. This matters for several reasons in the context of a subdivision strategy.

- First, it allows the seller to present a program, “I have a /16 I will be subdividing into /22s over the next several months”, rather than executing in an ad-hoc manner.

- Second, it allows for fee negotiation, including the possibility of reduced IPv4.Global fees for larger or structured engagements, which can meaningfully affect the economics of multi-transaction programs.

- Third, it provides access to the brokerage team’s expertise on pricing, timing, RIR-specific compliance, and buyer identification, effectively outsourcing the operational complexity described above.

Other brokers in this market include IPXO, which operates primarily in the leasing space but also facilitates purchases and the Brander Group, which focuses on the North American market. There are also several regional specialists in RIPE NCC and APNIC space. For large-scale subdivision programs, comparing broker capabilities, fee structures, and access to buyer networks across these options is worthwhile. That said, IPv4.Global’s combination of marketplace depth, pricing transparency tools, private sales capability, and documented expertise in navigating multi-RIR compliance makes it the strongest starting point for most sellers considering this strategy.

Modeling the Opportunity: An Example

Consider a /16 block registered under RIPE NCC, sold as a single block at current market pricing of approximately $12-15 per address. At 65,536 addresses, the revenue from this sale is $785,000-$983,000. IPv4.Global’s brokerage fee on this transaction of 2%-3% amounts to 1/IP brokerage fee on acquisition reduces this revenue by between $15,700 and $24,490. Net revenue to a seller would be approximately $750,51-$967.300, before any RIR fees (which are zero for RIPE transfers for sellers).

Then consider if the /16 is subdivided into sixty-four /22 blocks of 1,024 addresses each. At current /22 pricing in RIPE NCC space of approximately $30-35 per address, each /22 sells for $30,720-$35,840. IPv4.Global’s fee to expedite this transfer is, of course, negotiable. But, in a typical scenario of 4%, the fee per /22 block would be larger, with the total for all 64 blocks ranging between $76,643-$91,750. Under this scenario, the seller’s net revenue by subdividing the /16 is approximately between $1,887,000 and $2,202,000.

The spread before any residual costs is clearly over $1 million.

The risks and qualifications are significant: pricing may move during the execution period; not all /22s may sell at full prevailing rates; execution takes time and operational effort; not all /16s will have clean transfer histories; and the math changes in non-RIPE registries, though not significantly. This is an illustration of the opportunity’s upper bound under favorable conditions, not a guaranteed outcome.

Timing and the Window

Markets reprice. The 2020-2021 window advantaging subdivided large blocks closed for a number of reasons including when sellers recognized the opportunity and began subdividing, normalizing the gap. The current spread, historically wide, has already attracted notice. IPv4.Global and multiple market commentators have explicitly flagged the subdivision opportunity in recent reporting.

That doesn’t mean the window is closed, but it means it is not infinite. The more large block holders recognize this opportunity, the more that incremental supply of small blocks will moderate the pricing premium those blocks currently command.

Transaction volumes are at or near record highs. The market is liquid. Buyer demand for small blocks is durable. The conditions for this strategy are present today in a way they haven’t been since 2021. Whether that remains true in twelve months depends on how quickly market participants move.

The practical takeaway is simple: if this strategy interests you, the time to evaluate it seriously is now, not after watching another year of price data. The tools to do so, IPv4.Global’s fee calculator, pricing history database, and private sales team, are available and designed precisely for this kind of analysis.

Conclusion

The IPv4 large-block subdivision strategy is not new, but it is newly viable again, and by some measures more attractive than its first iteration. Large blocks are at multi-year pricing lows. Small block demand is stable. The spread between them is historically wide. The infrastructure of the secondary market, brokerages, transfer expertise, pricing data, and buyer networks, is more developed than it was in 2020.

The constraints are the same as they always were: transfer costs that vary materially by RIR, operational complexity that rewards those with or who can access genuine expertise, and the need for a robust buyer pipeline. Navigating those constraints intelligently, structuring the right brokerage relationship, and negotiating fees with both costs and benefits in mind, are what separates the IPv4 holders who capture this opportunity from those who may regret missing the opportunity in 2027.

The block flip is back. The math is there. The question is whether you have the execution to match.